This article is only available to Macro Hive subscribers. Sign-up to receive world-class macro analysis with a daily curated newsletter, podcast, original content from award-winning researchers, cross market strategy, equity insights, trade ideas, crypto flow frameworks, academic paper summaries, explanation and analysis of market-moving events, community investor chat room, and more.

Every week, we bring together our community of macro experts to discuss the latest market developments. In this piece, we distil the insights from our conversations up to 23 May. These are views from our network rather than the views of the Macro Hive research team. ‘[Day]’ indicates the day the comment was made.

A Conversation on Inflation Dynamics

- Member One: Given so many of the one-off forces that boosted global potential GDP are ending, and there are shocks on top of this, we have to fundamentally reduce the money-supply backing the system by a vast quantity, or expect a huge increase in inflation. So central banks cannot increase supply, but they do need to rebalance money supply in a dramatic way. Set it against a backdrop of a vast global and USD priced debt, and we’re in a very unfortunate situation to say the least.

- Member Two: But the money supply, as in the Fed’s balance sheet, does not really enter the economy and does not have an outsized effect on goods/services inflation directly. It does have a huge effect on asset price inflation though.

- Member One: I agree. Post-GFC, QE was a swap function only, but it ultimately restored the health of the banking system, so it can now create loans in a very healthy dose. The fiscal/central bank interaction has enabled huge deposit creation and the stability has enabled the collateral system to be maxed out. The offshore Eurodollar system has ballooned on low US rates, and that’s pure ledger money. Then add on the asset appreciation, house prices etc., and the money cycle has been crazy.

- Member Two: It is possible that borrowing picks up and thus money supply picks up. But the data does not show an extraordinary rise in borrowing post-COVID, and Member Two doubts it will ahead (as interest rates are rising). They like looking at FRB H.8 (commercial banks) balance sheets as they have used the extra deposits to buy securities (up 44%) while loans and leases are up just 4% (in comparison to April 2020). Since GFC, securities on banks’ balance sheets are up 175%, loans and leases are up 62%.

US

Month-end US equity flows

- A twitter user claims Morgan Stanley is estimating that $34bn will flow into US equity for month-end flows.

- There’s so much inflow to keep institutional allocations to equities stable following a 15-to-20% decline since last month, with the money coming from bonds.

- It could also be MSCI rebalancing. This time there is a lot of US companies being added versus other countries being removed. Last year there were quite a few Swedish companies added and EUR/SEK had a very large down move at the 4PM month-end fix.

Europe

Ending the reliance on Russian oil and gas

China

Did the cut to the five-year prime rate matter to the property market?

- It’s one of a series of targeted micro-measures that the PBoC have taken to support property. Others are an increased loan-to-value (LTV) ratio, improving credit access for people, etc. These measures should have some effect when lockdowns end. For developers, there has been some relaxation of last year’s measures, but the main measure (i.e., the three red lines) hasn’t been relaxed. It means state-owned enterprises could take over all private developers.

- House prices in tier one and tier two cities will be okay, prices will not necessarily go down. Recall these cities saw prices going up until Q1. The government will make sure they remain stable. But tier three cities and the countryside are drifting lower. In short, there is currently an uneasy status quo in the housing market.

Will China growth stabilise?

Renewable Energy

The excess of capital and low energy prices is giving all the wrong signals to the ‘technology solved everything’ view.

- The Energy Return on Energy Investment (ERoEI) cliff is likely the most important chart in energy economics and development (it shows the diminishing net energy return in renewable tech vs non-renewables). It’s almost the opposite of Moore’s law for technology [computational progress will become significantly faster, smaller, and more efficient over time]. It explains a lot of the collapse in productivity in US and Europe.

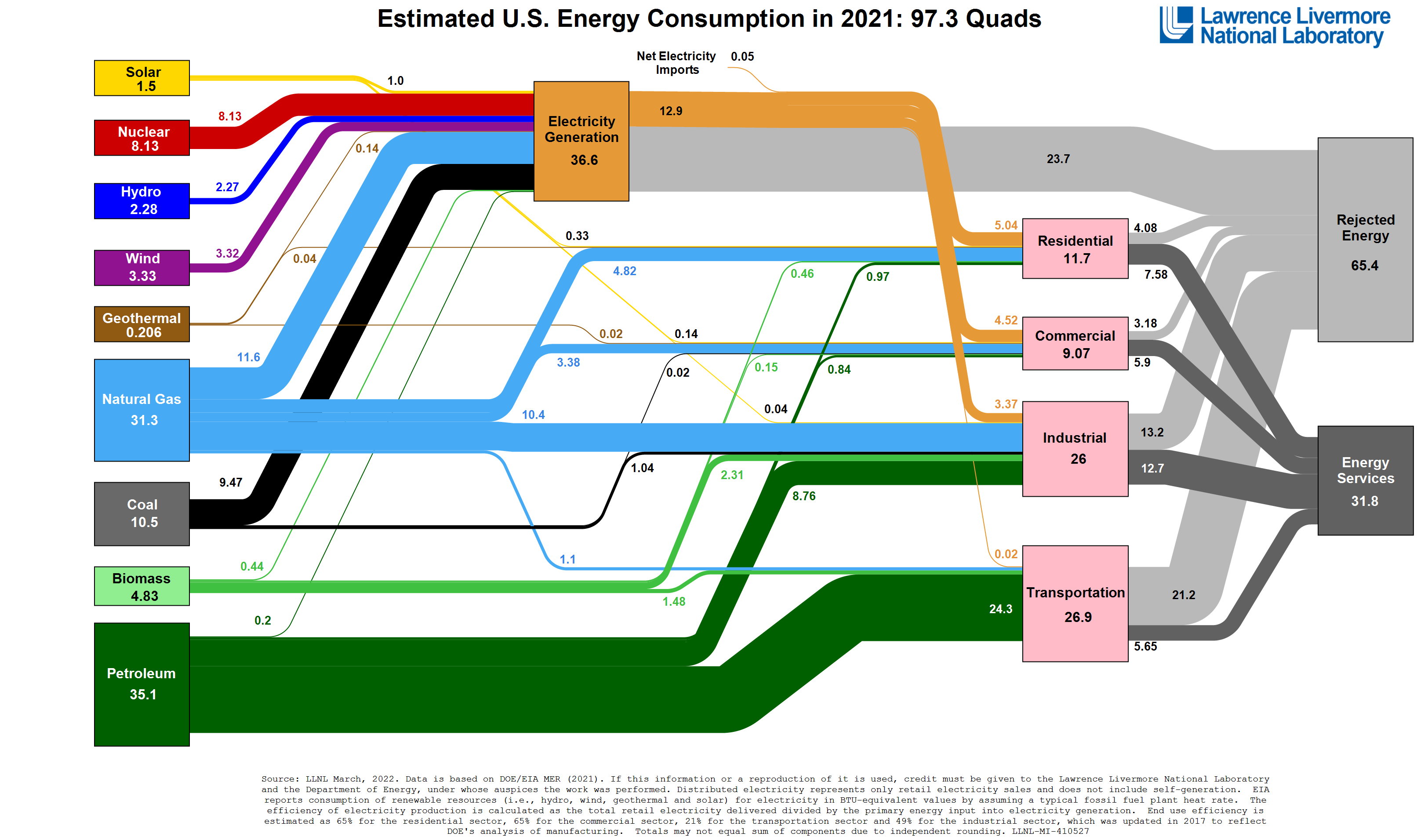

How has wasted energy evolved over time?

- Lawrence Livermore National Laboratory (LLNL) produces energy flow charts for the US economy. Wasted energy has risen from 50% in the 1960s to 65.4% – basically declining EROEI. A big jump in wasted energy came in 2011 because of shale oil and gas. A similar jump happened in the 1970s when the US shifted production back home after the oil crises and thus moved down the EROEI cliff. The UK has a much lower percentage of wasted energy than the US [2017 numbers show UK waste 46.5%].

The State of the Global Housing Market

Anecdotal evidence

- The rental markets in London and NYC have gone ballistic. A three-bed apartment in Queens Gate, South Kensington, came off a one-year lease and its rate went from £12k/month to £21k/month.

- One of our network is looking to rent in NYC and noted that anything reasonable listing will close instantly. The story that everyone had left NYC for Miami seems to just be a story.

- Another in our network states that rent prices take a while to flow through. They have a few rental properties in NYC and said that most leases give current tenants an option to renew for a year at about a 10% increase. Everyone has taken the option instantly, which suggests the market is higher. Will take time to flow through to inflation numbers though.

A Case to Sell Luxury Brand Stocks?

One of our network has gone short LVMH and wants to sell more luxury names

- They reasoned that the average person checks their statements relatively infrequently and probably haven’t seen much change yet. A bit more stress and your statements become far small. Then you might hold off purchasing your next luxury item.

Why luxury? These brands are not average shops, they’re not for the average person

- The level of sales of these brands is not only sustained by the ultra-rich. It has been sustained by the wide participation of people stretching for their luxury goods you would probably find. Even for the people with money, their broker statements will come in looking far worse than usual. One of the first things to go is the expensive accessory. Moreover, add to that the rampant inflation of these goods, you can argue that they should take a decent hit. Now Watches of Switzerland have raised their guidance and said the demand for their most expensive watch is still unmet.

Trade Ideas

- Short GBP [Wednesday]. Sell GBP rallies.

- Long EUR/USD [Wednesday]. Target and Walmart news looks bad. They think the market could increasingly price stagflation in the US.

- Constructive EUR [Saturday]. ECB liftoff in July with 50bps is possible; Macron’s blueprint for changes to European constitution, supported by Scholz; Ukraine could defeat Russia or force a cease fire; US financial conditions are being tightened via lower equity markets, while rate differentials have peaked; China ends lockdown.

Is loose fiscal and tight monetary policy good for GBP?

- Our network thinks so. But one makes the point that monetary policy isn’t tight, thus it’s bad. They do concur that the market will more likely think like our network though.

Market Fundamentals

- It seems the China view has changed from ‘decline’ to ‘bottomed and maybe gradually improving’. So, to the extent that CNH/China stops spooking everyone, there could be some upside in commodity FX that were doing so well in Q1 but then got blown up by China.

Price Targets

- S&P500: 3,600 might be the next washout target.

- EUR/USD: < 1.00

- GBP/USD: 1.15

- AUD/USD: 0.65

- Bitcoin: $20,000. They think if you can break at $28,000, then $20,000 seems like an easy journey.

Read, Listen, and Watch

Read

Listen

Bilal Hafeez is the CEO and Editor of Macro Hive. He spent over twenty years doing research at big banks – JPMorgan, Deutsche Bank, and Nomura, where he had various “Global Head” roles and did FX, rates and cross-markets research.

Ben Ford is a Researcher at Macro Hive. Ben studied BSc Financial Mathematics at Cardiff University and MSc Finance at Cass Business School, his dissertations were on the tails of GARCH volatility models, and foreign exchange investment strategies during crises, respectively.

(The commentary contained in the above article does not constitute an offer or a solicitation, or a recommendation to implement or liquidate an investment or to carry out any other transaction. It should not be used as a basis for any investment decision or other decision. Any investment decision should be based on appropriate professional advice specific to your needs.)

Enter your email to read this Macro Hive Exclusive

OR

START 30-DAY FREE TRIAL

Already have a Macro Hive Prime account? Log in

{kind=link}