With Prime Minister Boris Johnson unveiling a new three-level alert system, we look at the ongoing COVID-19 developments in the UK.

Cases and Deaths

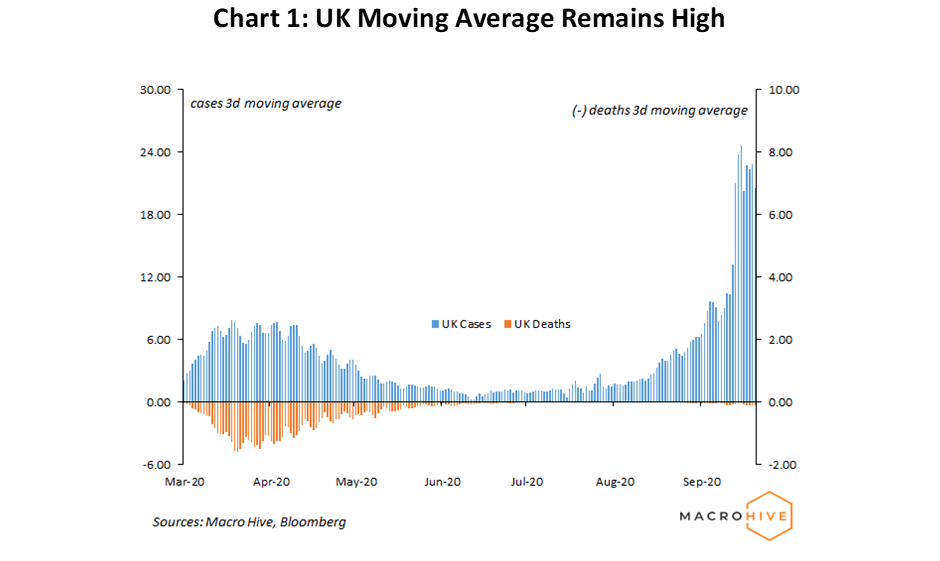

The UK has registered 100,000 cases over the last seven days, a 48% rise WoW. This is equivalent to 149 cases per 100,000 population, a rise similar to France (158). New infections have, however, stabilised (Chart 1). The weekly change in 3d moving average is -2%.

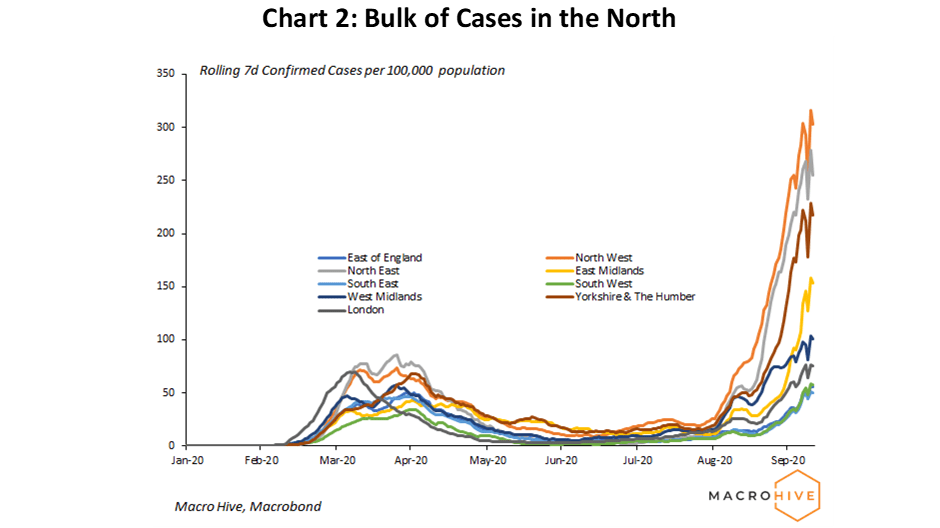

The majority of positive tests have been confirmed in Northern England, with the North West, North East and Yorkshire regions accounting for just under half of cases across the UK (Chart 2).

Hospitalisation and Testing

As the number of cases has risen, so has the number of hospital admissions (Chart 3). Total COVID-19-related admissions rose to 3,800 on 8 October, a 50% WoW rise. The three-week lag in hospital admissions implies that, if admissions rise at the same rate as new infections have over the last three weeks, we could see total hospital admissions reach 15,000 by November. Nightingale hospitals in the North have been placed on alert.

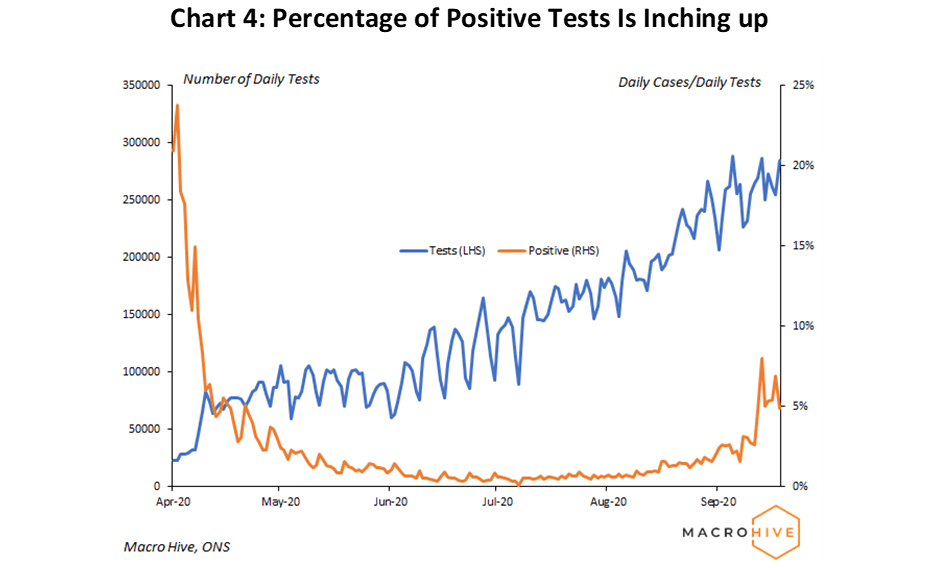

Over the last week, an average of 270,000 tests were performed each day. The percentage of positive tests is also starting to rise (Chart 4).

Mobility

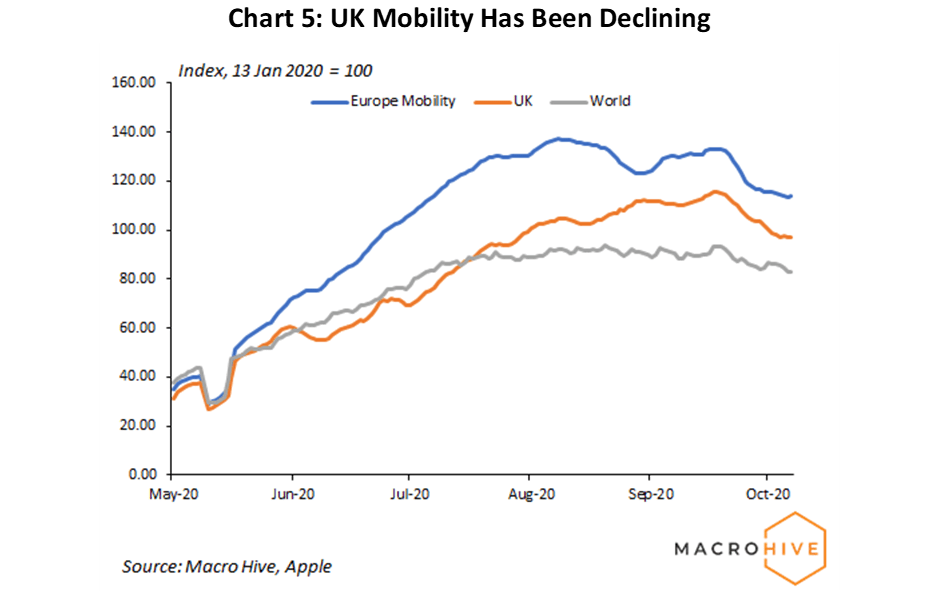

As local measures begin to become more stringent, mobility has started to fall across the UK (Chart 5). Since the end of September, the fall in mobility has been more pronounced in the EU and UK compared to other countries around the world. We would expect there to be a small decline in mobility after the holiday season, but the excess decline is at least in part due to rising cases.

Implications

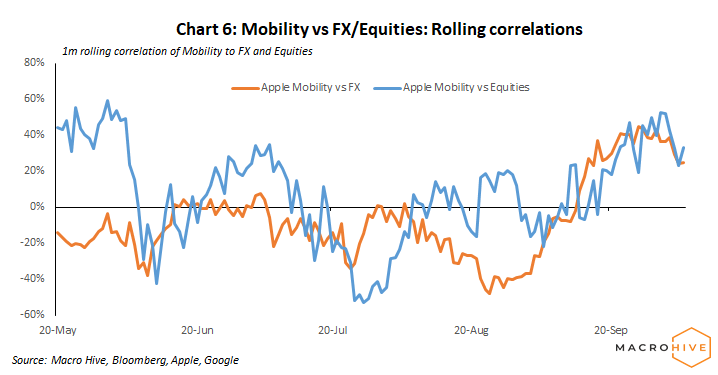

We publish a weekly Macro Risk Scorecard which pulls together all our COVID-related data from cases/deaths to mobility and stringency policies. Last week, Apple mobility was correlating positively with FX/Equities (Chart 6). That is, lower WoW mobility is correlated to weaker FX and stock performance.

The reluctance of European governments to impose stricter lockdowns captures the trade-off between loss of economic activity and protecting public health. The data in this note shows that the UK public health situation is deteriorating. If this translates into more stringent lockdowns and lower mobility, we could realistically expect this to trickle through into economic activity. This inevitability is perhaps what is driving the Bank of England to think about the feasibility of negative rates.

Sam van de Schootbrugge is a macro research economist taking a one year industrial break from his Ph.D. in Economics. He has 2 years of experience working in government and has an MPhil degree in Economic Research from the University of Cambridge. His research expertise are in international finance, macroeconomics and fiscal policy.

(The commentary contained in the above article does not constitute an offer or a solicitation, or a recommendation to implement or liquidate an investment or to carry out any other transaction. It should not be used as a basis for any investment decision or other decision. Any investment decision should be based on appropriate professional advice specific to your needs.)