Monetary Policy & Inflation | US

FOMC Preview: Steady as She Goes

- By Dominique Dwor-Frecaut

- Sign-up to discuss on Slack

- 4 min read

Monetary Policy & Inflation | US

Since the December meeting, little has changed on growth and inflation. Growth has continued to slow, if faster since early January when Omicron’s impact strengthened, and the slow disinflation started in Q4 has continued. Consequently, the Fed’s stance has likely changed little since the December meeting.

I expect the Fed to maintain the current schedule of asset purchases, i.e., to end in March. Several investors have found the continuation of purchases inconsistent with hawkish talk and current hints at a March hike. I agree but think it reflects the very large scale of QE, which the Fed believed it could not shut down at short notice without upsetting markets.

I expect the taper to still end in March for two more reasons. First, the Fed is the Treasury’s investment banker, and a key tenet of the Treasury debt policy, and by association of quantitative easing (QE), is predictability. Second, the Fed wants to avoid looking rushed as that could imply it is behind the curve.

A March liftoff would align with recent FOMC members’ chatter and the December Summary of Economic Projections (SEP). To justify a March liftoff, Powell will likely maintain a cheery outlook and dismiss the recent economic weaknesses as Omicron related and unlikely to last.

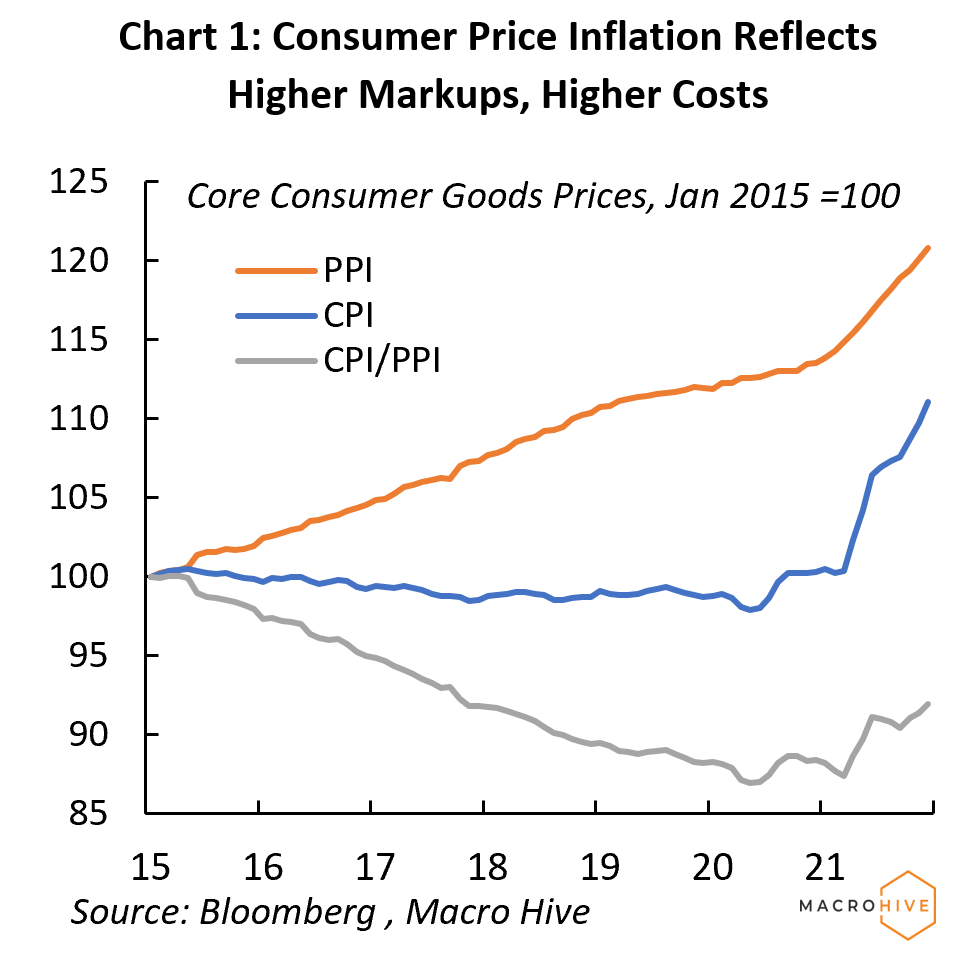

I base this on my inflation view. Despite improvements in supply, profits have remained high, reflecting strong corporate market power. Lower costs are fattening the bottom line of large corporations rather than getting passed on to consumers (Chart 1). This suggests only a gradual decline in inflation, unless the US economy experiences a demand contraction large enough to reduce firms’ market power. That is possible but more likely in H2 than H1.

For the second round of quantitative tightening (QT2), the Fed will likely follow its usual playbook. It will probably introduce policy tightening very gradually to avoid upsetting markets. Powell mentioned casually during the December presser that ‘we had our first discussion about the balance sheet, for example’ (the reporters present ignored him). The minutes then mentioned QT more formally, providing the broad contours:

I expect Powell to hint that QT2 could start around midyear, based on a recent statement that 2-4 discussions would be needed to finalize QT2 details. A recent article by The Wall Street Journal reporter Nick Timiraos, often an unofficial Fed voice, said ‘the turn from expanding the portfolio to contracting it is likely to be measured in months and not years’.

Markets underestimated the Fed hawkishness after the December meeting. And as much as they did, they could now be overestimating it or, rather, overestimating its market impact. Markets are currently pricing four hikes in 2022, my base case scenario. But that is not an aggressive tightening plan: the real Fed Funds rate (RFFR) is currently -5.5%, the lowest since the 1960s. The end-2022 RFFR implied by the December SEP is -1.75%. Even if the Fed hiked five times in 2022, the end-2022 RFFR would still be below -1%. That is hardly the stuff of prolonged market selloffs.

These suggest the market selloff and curve tightening may not last. Also, while the meeting’s tone will likely remain hawkish, it could still assuage investors’ concerns over Fed hawkishness by providing further details on interest rates and balance sheet plans. Consequently, a rally in both bonds and stocks could follow the meeting.

Spring sale - Prime Membership only £3 for 3 months! Get trade ideas and macro insights now

Your subscription has been successfully canceled.

Discount Applied - Your subscription has now updated with Coupon and from next payment Discount will be applied.