This article is only available to Macro Hive subscribers. Sign-up to receive world-class macro analysis with a daily curated newsletter, podcast, original content from award-winning researchers, cross market strategy, equity insights, trade ideas, crypto flow frameworks, academic paper summaries, explanation and analysis of market-moving events, community investor chat room, and more.

Over August, there was pronounced dollar weakness, especially against NOK, AUD and CAD. This reduced NOK and CAD undervaluation, but increased AUD overvaluation (though it remains below the 20% extreme). In EM, CNH, MYR and MXN saw the biggest gains, while TRY and BRL moved deeper into undervaluation territory. Below are the details. (We prefer to look at PPP and real trade weighted based valuation metrics as they have tended to be more reliable than BEER and FEER models).

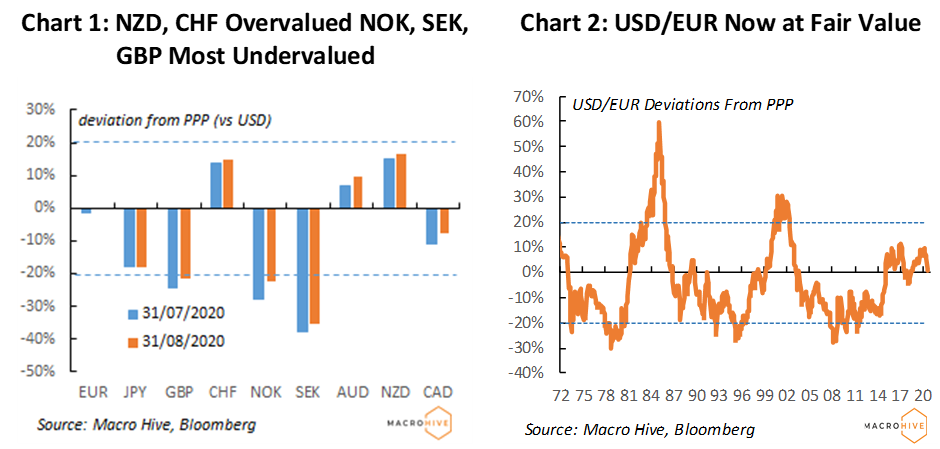

In G10

- SEK is the most undervalued currency. It has bounced off its undervaluation extreme, which suggests it could have further to appreciate (Chart 4). NOK and GBP are the other heavily undervalued currencies, though less so than before (Chart 1). The JPY remains stubbornly undervalued.

- NZD and CHF are more than 10% overvalued, while the AUD increases its overvaluation but at less than 10% (Chart 4).

- EUR/USD is now trading around fair value (1.20, Chart 2), while USD/JPY is still above fair value (90, Chart 3).

In EM

- TRY and BRL are heavily undervalued (Chart 5). That said TRY has tended not to exhibit clear mean-reverting behavior (Chart 6). However, RUB – the third most undervalued currency – does tend to mean-revert, so it could be an attractive buy (Chart 7).

- On the expensive side, HKD and TWD are hovering around the 20% overvaluation mark.