Friedman’s Plucking Model Is Back in Vogue, and Rightly So!

- By Julius Probst, PhD

- Sign-up to discuss on Slack

- 4 min read

Today, most central banks use Dynamic Stochastic General Equilibrium (DSGE) models for policymaking and forecasting. These models are founded on the New Neoclassical Synthesis, which merges key Keynesian elements with monetarist/neoclassical theories. But empirical evidence suggests such a theoretical underpinning may no longer be applicable – a view the Fed seemingly shares. We explain why.

Modern macroeconomic theory is largely built on the New Neoclassical Synthesis that emerged in the late 1980s. The synthesis combines key Keynesian elements with monetarist/neoclassical theories, and it now underpins the DSGE models that most central banks use for policymaking and economic forecasts.

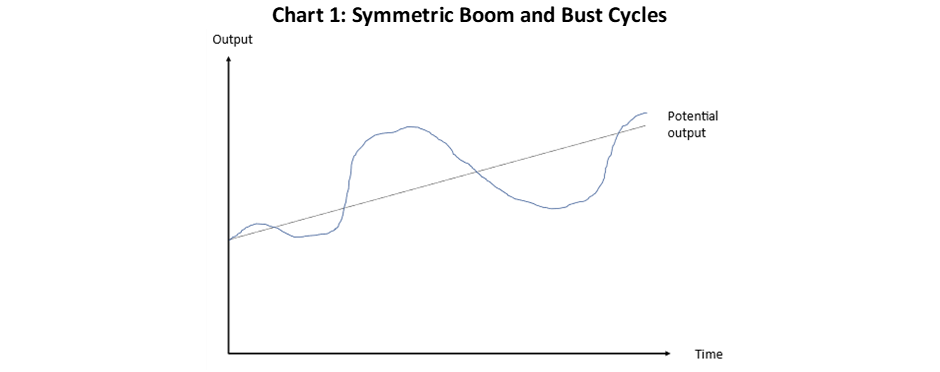

Central to the Neo-Keynesian model is that the business cycle is symmetric (Chart 1). And so, economic variables like the unemployment rate and GDP growth fluctuate in the short term (booms and busts) around what are assumed to be their natural rates. The natural rates are independent of demand-side factors, meaning that fiscal or monetary policy should not affect the economy’s long-run potential.

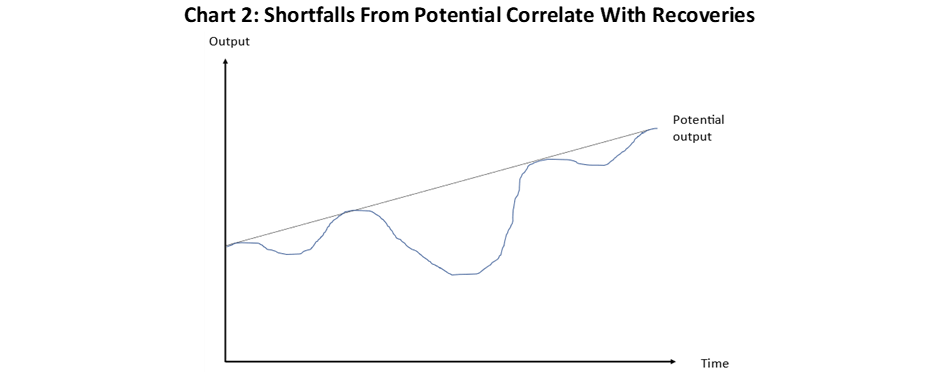

Alternatively, Friedman’s plucking model suggests that there are no booms. Instead, we only have shortfalls from potential where, say, output and employment are ‘plucked’ downwards from a ceiling value (Chart 2). Negative demand shocks drive these short-term drops, but supply-side factors, like tax and regulatory policies, or changes in productivity growth can also move the economy’s long-run potential.

Regarding short-term dynamics, the plucking model assumes the size of economic downturns correlates with the size of subsequent recovery phases. In other words, the sharper the downturn, the quicker the recovery. However, unlike in the Neo-Keynesian model, the size of the previous recovery does not predict the size of any future downturn.

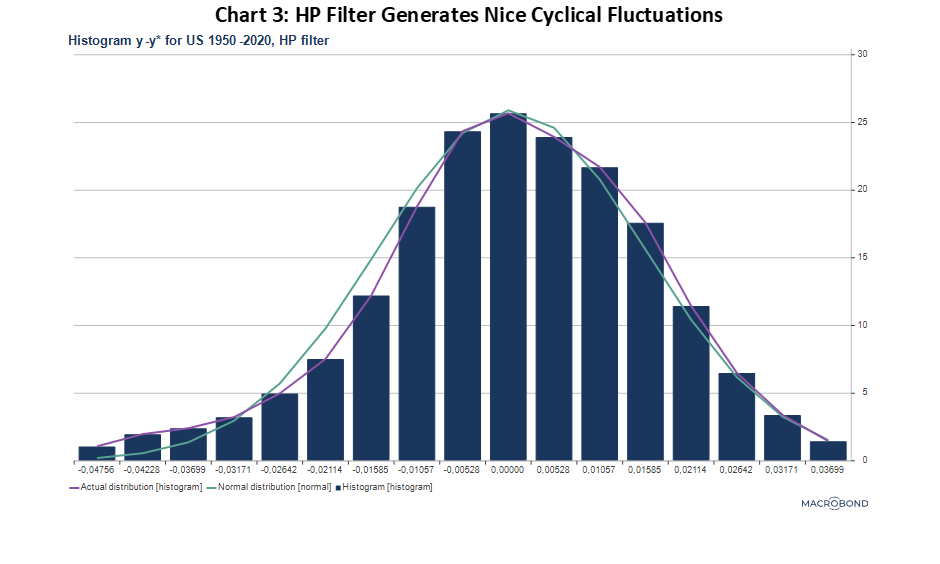

Historically, macroeconomists have turned to the Hodrick-Prescott (HP) filter to estimate the economy’s potential capacity and calculate output gaps. In essence, this method extracts a cyclical dynamic (typically eight years for US GDP) from noisy data, leaving behind smooth longer-frequency fluctuations. By design, it produces an output gap over time that follows the normal distribution with a mean of zero (Chart 3). The issue is that this can create spurious cycles, generating (for example) strong positive output gaps before any large macroeconomic downturn, even if there was little evidence of an economic boom at the time.

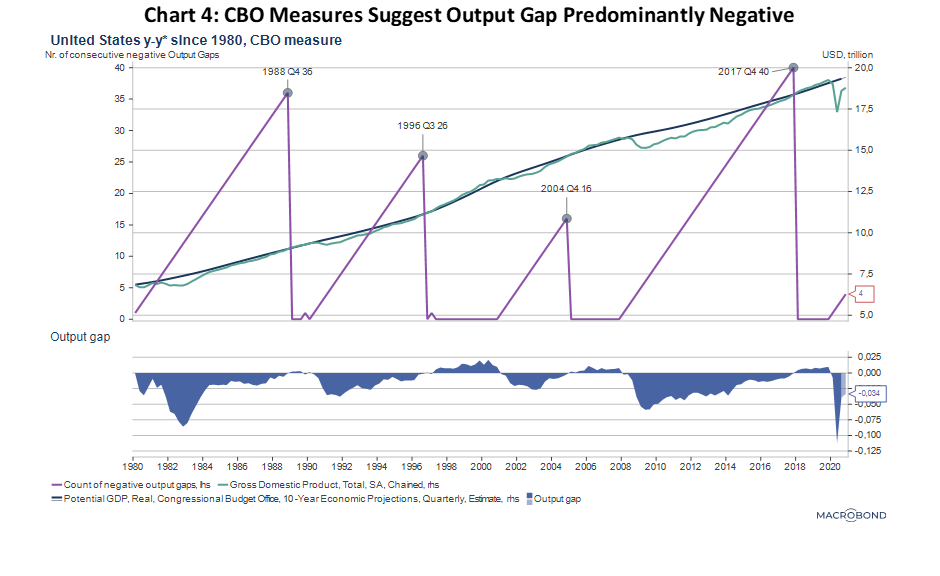

Output gaps are far less likely to follow similar business cycle fluctuations using other measures. The CBO uses a relatively sophisticated growth model that contains individual production functions for each sector. It obtains an estimate for the productive capacity of the US economy based on the capital stock and capital accumulation.

According to the CBO measure, the US economy has operated below full capacity for about 75% of the time since 1980 – some 124 quarters out of 164 in total since 1980 (Chart 4). Furthermore, the output gap distribution is highly skewed with a fat left tail, meaning that large negative output gaps are much more common than large positive ones, which barely seem to exist. Since 1980, the median (mean) output gap has been -1.3% (-1.6%), implying that the US economy has operated well below potential capacity for decades. And even the CBO measure might be quite conservative in these output gap estimations.

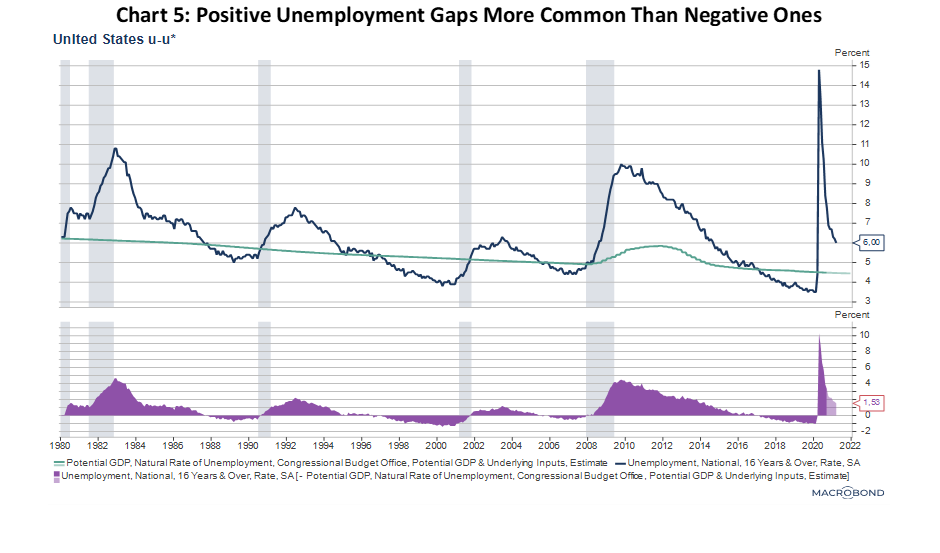

We can see a very similar phenomenon with unemployment. According to the CBO estimate, US unemployment has been significantly higher than its long-run natural rate in recent decades (Chart 5). The unemployment gap has averaged about 1% each month since 1980. Moreover, there is also severe positive skew in the distribution, meaning that positive unemployment gaps are much more common and also significantly larger than negative unemployment gaps.

This makes sense. Policymakers can only push unemployment marginally below its natural rate, whereas excess unemployment can potentially rise by 10% or more – as the recent Covid-19 shock and the Great Depression show.

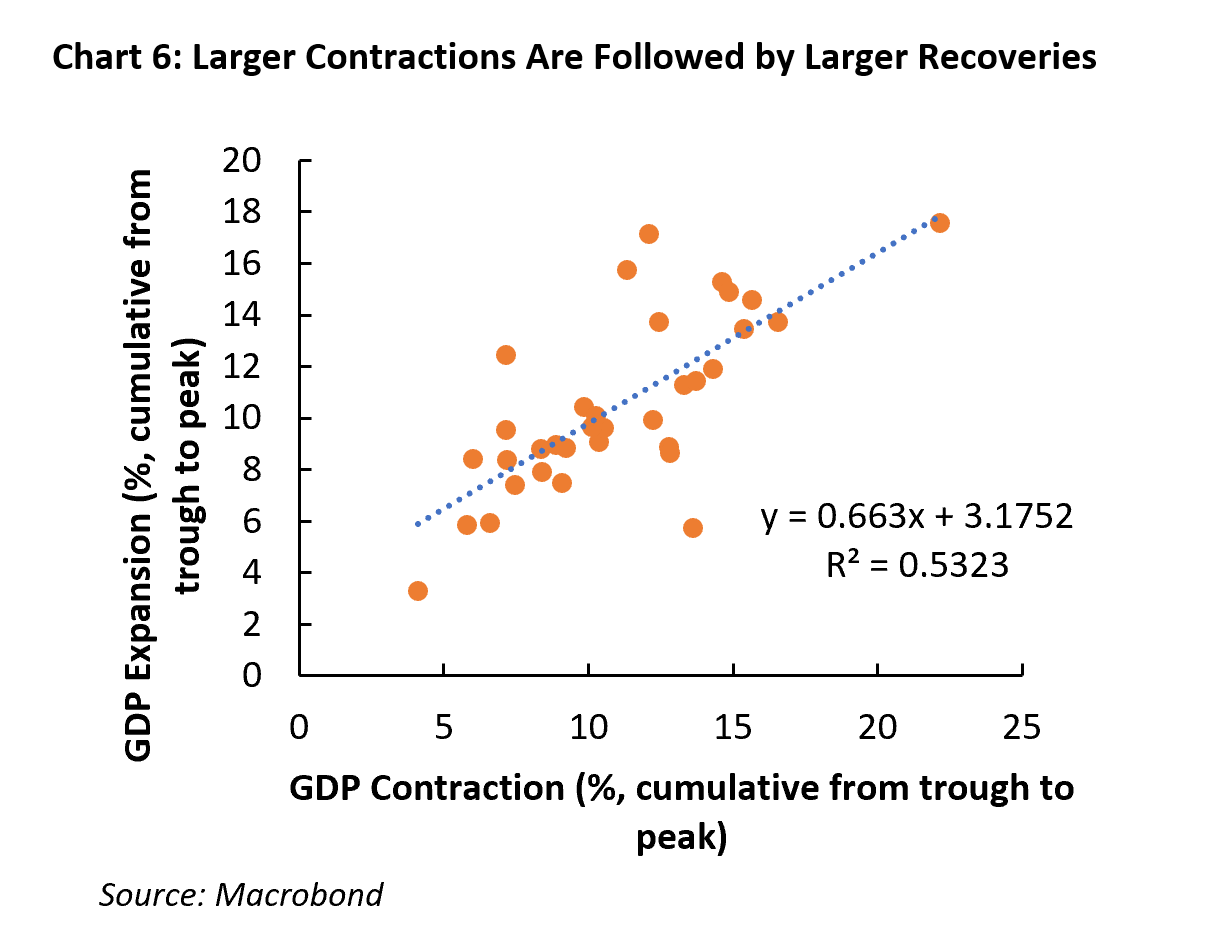

Lastly, the plucking property of the business cycle implies that larger macroeconomic slumps precede larger subsequent economic recoveries. Researchers have empirically confirmed this feature for the US business cycle and other advanced economies.

Using GDP data covering 34 OECD countries since the start of the pandemic, we find that there exists a clear correlation between the size of the economic contraction and the subsequent recovery (Chart 6). In accordance with Friedman’s plucking model, the size of the bust does therefore predict the size of the boom.

While the Covid-19 shock might be somewhat unique, GDP fluctuations during the Great Recession displayed similar features. Additionally, data rejects the Neo-Keynesian hypothesis that the size of the boom should predict the size of the subsequent economic downturn. So, the evidence appears to largely favour Friedman’s model. And it looks like policymakers might take notice.

If the CBO is correct, the Fed has been continuously underestimating the US’s full output potential in recent years. Their resulting tight monetary policy approach has produced an average inflation rate closer to 1.5% and led to prolonged high unemployment post 2008. Over a longer time horizon, an overly hawkish Fed stance could have contributed to the secular decline in the long-run real interest rate, a phenomenon many attribute to the secular stagnation hypothesis.

Recently, however, the Fed has apparently changed tack. In monetary policy statements, it dropped the term deviations from full employment in favour of shortfalls, seemingly dismissing the neo-Keynesian view and embracing Friedman’s hypothesis. Also, it introduced the new AIT framework, promising to allow inflation above 2% in the short to medium term. Such overshooting could be highly desirable if it makes up for previous policy mistakes.

The change comes just at the right time, and we can thank economists Paul Krugman, Lars Svensson, and former Fed Chair Ben Bernanke for the move. With the recent pandemic-induced shock, we have again entered an economic phase where millions of people recently lost their jobs. The US economy will experience substantial shortfalls from full employment in the foreseeable future. The move to the ‘plucking view’ will ensure such shortfalls are soon eliminated.

Spring sale - Prime Membership only £3 for 3 months! Get trade ideas and macro insights now

Your subscription has been successfully canceled.

Discount Applied - Your subscription has now updated with Coupon and from next payment Discount will be applied.